Investor Login

Investor Login

Weekly Newsletter #21/2015

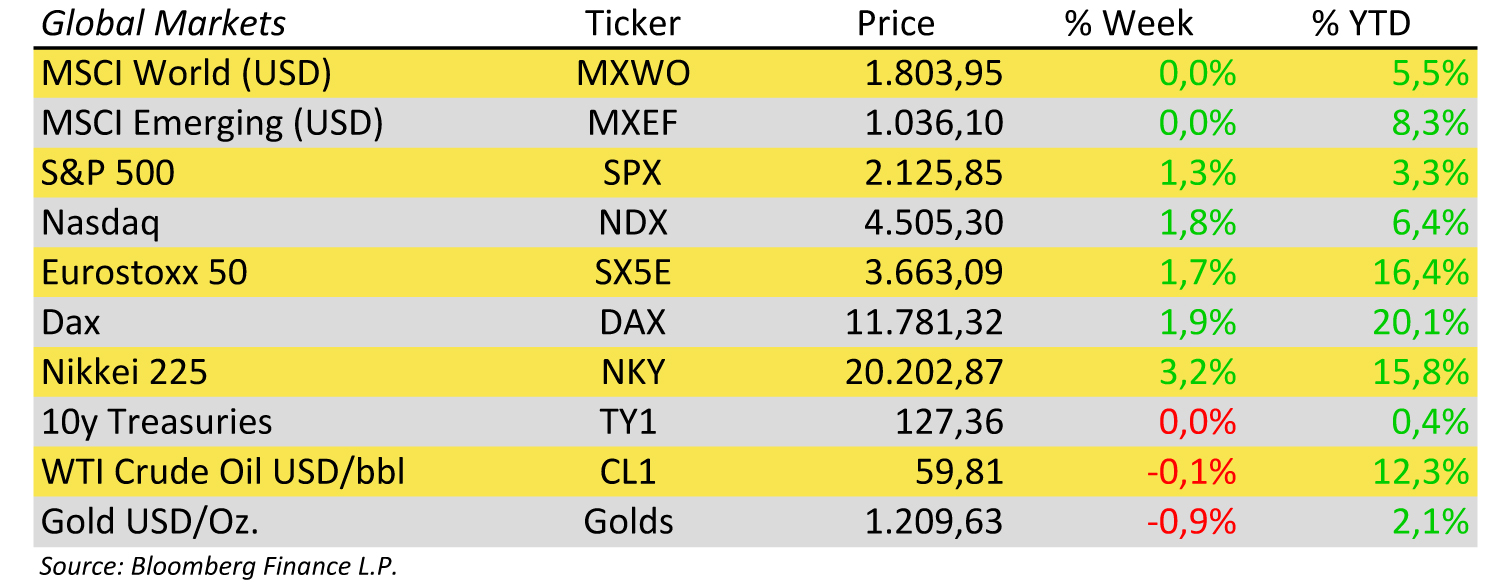

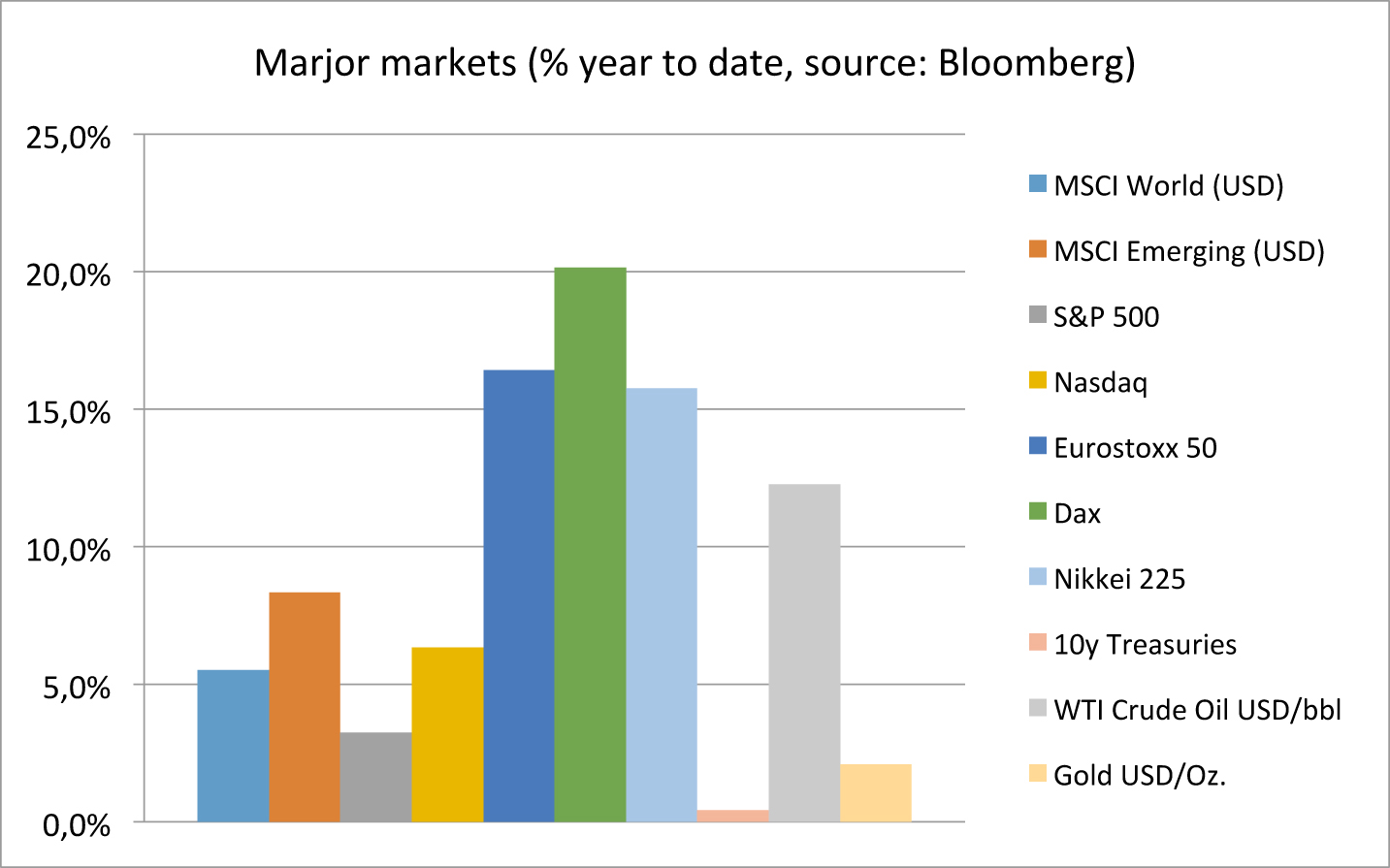

Versus our last report two weeks ago equity markets gained again while government yields were fairly stable. Taking a closer look at equities shows strong gains for European and Japanese equity markets, moderate gains for US markets and even a slight decrease for Emerging Markets.

U.S. Fed Minutes bolstered expectations that U.S. interest rates will remain near zero until later in 2015. Officials were concerned about soft consumer spending. Still most Fed members expect the U.S. economy to pick up pace after the slow first quarter.

Also the euro area’s economic recovery stuttered in May as Germany lost momentum, while weakness in China’s manufacturing industry persisted. The Markit index of services and manufacturing slipped for both the Eurozone and China. While it is for the Eurozone still on expansion level, it indicates for China contraction for five of the past six months. See also our chart of the day.

Erwin Lasshofer says the U.S. were probably the best-performing major economy in the world. However the resulting capital inflows have driven prices higher. Thus it is important to screen global markets for opportunities. See also our product offer with German and Australian stocks.

Archives

- June 2019 (1)

- March 2019 (1)

- February 2019 (1)

- December 2018 (1)

- May 2018 (1)

- January 2018 (1)

- December 2017 (2)

- October 2017 (1)

- September 2017 (1)

- August 2017 (1)

- July 2017 (1)

- June 2017 (2)

- May 2017 (2)

- April 2017 (2)

- March 2017 (3)

- February 2017 (2)

- January 2017 (2)

- December 2016 (4)

- November 2016 (3)

- October 2016 (3)

- September 2016 (2)

- August 2016 (5)

- July 2016 (2)

- June 2016 (4)

- May 2016 (1)

- April 2016 (4)

- March 2016 (5)

- February 2016 (3)

- January 2016 (3)

- December 2015 (5)

- November 2015 (5)

- October 2015 (4)

- September 2015 (3)

- August 2015 (7)

- July 2015 (7)

- June 2015 (5)

- May 2015 (6)

- April 2015 (9)

- March 2015 (9)

- February 2015 (9)

- January 2015 (9)

- December 2014 (11)

- November 2014 (10)

- October 2014 (3)

- September 2014 (1)

- August 2014 (2)

- July 2014 (2)

Related Posts

Weekly Newsletter #17/2015

By Erwin Lasshofer

What would you expect a risk-market to do, if the investors are confronted with weak economic data?! Well, I bet you first answer is, that you expect the market to go down. And that is the only logical answer you can give. But in nowadays markets you probably would not win a lot of money […]

READ MORE

Weekly Newsletter #18/2015

By Erwin Lasshofer

After reaching new record highs global equity markets have been experiencing a slight correction. US GDP growth was a disappointing 0.2% for the first quarter this year. Market analysts expected 1.0% after reported 2.2% and 5% in the quarters before. Slow US growth raises the questions for US interest rates hikes again. US Fed […]

READ MORE

Weekly Newsletter #19/2015

By Erwin Lasshofer

The dollar sank and U.S. stocks fell to a one-month low after data on jobs and productivity added to concern economic growth is not robust enough. U.S. crude stockpiles fell by 3.88 million barrels last week while most analysts predicted an increase in supplies. Refineries operated at the highest rate in four months as imports […]

READ MORE