Investor Login

Investor Login

Weekly Newsletter

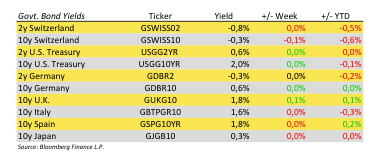

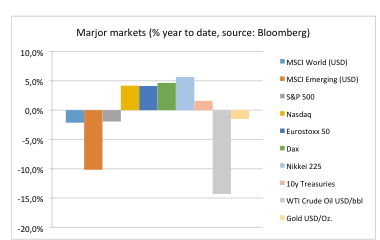

Markets are taking a breath after the quick recovery in early October.

The earnings reporting season had a satisfying start. About one-third of the major companies in the US and Europe have reported so far. In both regions they met sales expectations on average and bet earnings expectations slightly which means still a decline of earnings by about 6%!

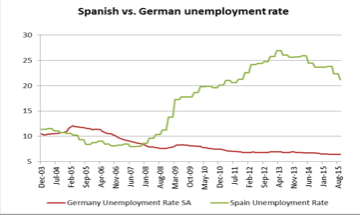

China GDP growth has been reported at 6.9% versus last year which is also above expectations, however marks a historic low and raises questions of overstatement by Chinese authorities. Good news from Europe: Spanish unemployment finally fell below 5 million which is a sign of European recovery although this level is still twice the amount before financial crisis. Compare to German unemployment rate at record low in our chart of the day.

So overall economic activity is fairly stable. The US is doing good, China is slowing down and Europe has a some recovery potential. The ECB is expected to extend its bond buying program in the fact of threatening deflation.

Erwin Lasshofer and his INNOVATIS still do not expect rate hikes any time soon. US inflation is low, the US dollar is strong and the rest of the world rather slow.

Archives

- June 2019 (1)

- March 2019 (1)

- February 2019 (1)

- December 2018 (1)

- May 2018 (1)

- January 2018 (1)

- December 2017 (2)

- October 2017 (1)

- September 2017 (1)

- August 2017 (1)

- July 2017 (1)

- June 2017 (2)

- May 2017 (2)

- April 2017 (2)

- March 2017 (3)

- February 2017 (2)

- January 2017 (2)

- December 2016 (4)

- November 2016 (3)

- October 2016 (3)

- September 2016 (2)

- August 2016 (5)

- July 2016 (2)

- June 2016 (4)

- May 2016 (1)

- April 2016 (4)

- March 2016 (5)

- February 2016 (3)

- January 2016 (3)

- December 2015 (5)

- November 2015 (5)

- October 2015 (4)

- September 2015 (3)

- August 2015 (7)

- July 2015 (7)

- June 2015 (5)

- May 2015 (6)

- April 2015 (9)

- March 2015 (9)

- February 2015 (9)

- January 2015 (9)

- December 2014 (11)

- November 2014 (10)

- October 2014 (3)

- September 2014 (1)

- August 2014 (2)

- July 2014 (2)

Related Posts

Weekly Newsletter

By Erwin Lasshofer

Global Markets have little changed since our last report two weeks ago. We do not expect this to change over summer time and will reduce our newsletter frequency to twice a months until we see a wake up or even shake up. However what we do not change is our effort to continuously look […]

READ MORE

Weekly Newsletter

By Erwin Lasshofer

The Greek Tragedy Greece has been dominating the headlines for a few weeks again. Clashes between the Mediterranean nation and its creditors shake up markets. Currently they are discussing continuous issues of sales-tax rates, pensions and budget deficits. Background In 2009 Greece revealed a deficit that was four times what the euro […]

READ MORE

Weekly Newsletter

By Erwin Lasshofer

Despite Greece is still dominating political and economic headlines nothing much has changed versus our last newsletter two weeks ago. Greece still wants to keep the Euro. The Troika of EU, ECB and IMF wants to keep Greece as a partner. Creditors do not want to write off their billions of money they lend to […]

READ MORE