Investor Login

Investor Login

Weekly Newsletter

The Greek Tragedy

Greece has been dominating the headlines for a few weeks again. Clashes between the Mediterranean nation and its creditors shake up markets. Currently they are discussing continuous issues of sales-tax rates, pensions and budget deficits.

Background

In 2009 Greece revealed a deficit that was four times what the euro rules allowed. Greece received a total of 240 billion euros in EU and IMF funds and forced creditors to write off 100 billion euros of privately held bonds. In return lenders pushed for spending cuts and an overhaul of everything from labor rules to taxi licensing.

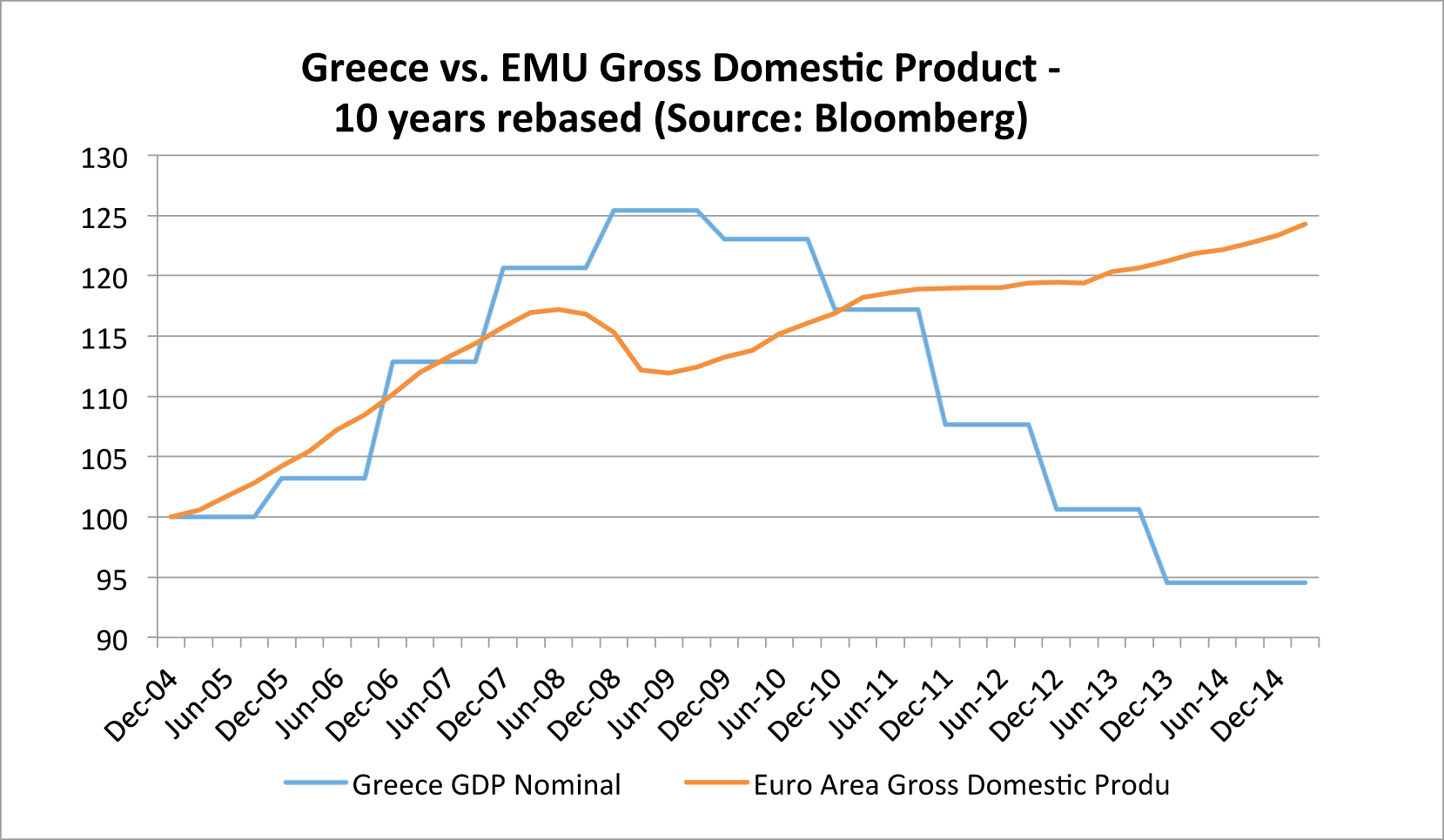

Accordingly 255’000 government employees were laid off, retirement age was raised from the lowest to the highest levels in Europe and the budget deficit has been decreased rapidly despite increasing social spending. During the following years unemployment tripled, youth unemployment reached even 60 percent and the Greek GDP fell by one quarter. This equals about the magnitude of the Great Depression in the 1930’s. See our chart of the day for a comparison of Greek vs. Euro Area GDP for the last ten years.

In January Greek Prime Minister Tsipras came to power on a promise to undo the economic medicine that shrank its economy. He quickly had to backtrack from writing off some off its 320 billion euro debt. However he reached an four-month loan extension, but only on the condition to comply closely with the existing bailout deal.

Current Situation

Many economists agree with Tsipras that Greece’s debt is too large for it to pay. Even the IMF said that for new budget targets to achieve sustainability, significant new financing and debt relief would be needed. On the other hand Europe won’t discuss debt relief until Greece has put its public finances on a sustainable footing.

Economic development in Greece is a huge challenge for its leaders. Greece’s debt is even further increasing relative to its shrinking economic power. Even worse it is a threat to democracy in a European country that was ruled by a Military Junta just 40 years ago.

European leaders are afraid of the moral hazard caused by an easy-going handling of the situation. While they could afford to bailout Greece again they could not afford to do so for Spain, Italy or even France. And they need to offer Greece an incentive not to demand continuous subsidies as a bailout or in another way.

The rest of the world such as the U.S. and or the IMF are afraid of turbulences at financial markets spilling over to them. Thus they push Europe for a quick solution of the situation.

Outlook for Greece

A debt cut appears inevitable. Greece economic situation is disastrous and the debt way to high to be repaid. Greece and the IMF want this to happen soon. Europe as the main lender prefers to avoid it as long as possible and may be able to do so. That’s why Erwin Lasshofer and his INNOVATIS team expect some sort of compromise and no material change of the situation.

Will Greece leave the Euro? The European Monetary Union was designed as a one-way road. There is no easy way out. On the long run a “Grexit” might help Greece to regain international competitiveness by devaluing its own currency. On the short run it might cause chaos and an even more economic sacrifice. We expect Greek’s political leaders to focus on the short run, i.e. keeping the euro. This is also preferred by the majority of Greek voters.

Other Options? The European Monetary Union would need a common fiscal policy with internal transfers from rich to poor countries. While this is a matter of course inside European nations it will be hard to get acceptance from tax-payers of rich European countries.

Financial Markets Outlook

Financial markets seem to be fairly prepared. European investment fund managers have increased their cash allocation to a six-year high. We have already seen a drop of 10% in Europe since April and there is not much absolutely unexpected ahead so far. Major forecasters tracked by Bloomberg have not lowered their year-end estimates. UBS even increased it projection this month citing better than expected earnings growth and a turn in the economy.

Erwin Lasshofer expects some volatility in the short term until we have a deal with Greece. This might even further delay a possible rate hike by the Fed. In the unlikely event of a “Grexit” we expect European equity markets to drop 10-20% in the short term. In the long term we are positive and expect increasing markets.

Archives

- June 2019 (1)

- March 2019 (1)

- February 2019 (1)

- December 2018 (1)

- May 2018 (1)

- January 2018 (1)

- December 2017 (2)

- October 2017 (1)

- September 2017 (1)

- August 2017 (1)

- July 2017 (1)

- June 2017 (2)

- May 2017 (2)

- April 2017 (2)

- March 2017 (3)

- February 2017 (2)

- January 2017 (2)

- December 2016 (4)

- November 2016 (3)

- October 2016 (3)

- September 2016 (2)

- August 2016 (5)

- July 2016 (2)

- June 2016 (4)

- May 2016 (1)

- April 2016 (4)

- March 2016 (5)

- February 2016 (3)

- January 2016 (3)

- December 2015 (5)

- November 2015 (5)

- October 2015 (4)

- September 2015 (3)

- August 2015 (7)

- July 2015 (7)

- June 2015 (5)

- May 2015 (6)

- April 2015 (9)

- March 2015 (9)

- February 2015 (9)

- January 2015 (9)

- December 2014 (11)

- November 2014 (10)

- October 2014 (3)

- September 2014 (1)

- August 2014 (2)

- July 2014 (2)

Related Posts

Weekly Newsletter #19/2015

By Erwin Lasshofer

The dollar sank and U.S. stocks fell to a one-month low after data on jobs and productivity added to concern economic growth is not robust enough. U.S. crude stockpiles fell by 3.88 million barrels last week while most analysts predicted an increase in supplies. Refineries operated at the highest rate in four months as imports […]

READ MORE

Weekly Newsletter #21/2015

By Erwin Lasshofer

Versus our last report two weeks ago equity markets gained again while government yields were fairly stable. Taking a closer look at equities shows strong gains for European and Japanese equity markets, moderate gains for US markets and even a slight decrease for Emerging Markets. U.S. Fed Minutes bolstered expectations that U.S. interest rates […]

READ MORE

Weekly Newsletter

By Erwin Lasshofer

Global Markets have little changed since our last report two weeks ago. We do not expect this to change over summer time and will reduce our newsletter frequency to twice a months until we see a wake up or even shake up. However what we do not change is our effort to continuously look […]

READ MORE