Investor Login

Investor Login

Newsletter dated April 28, 2016

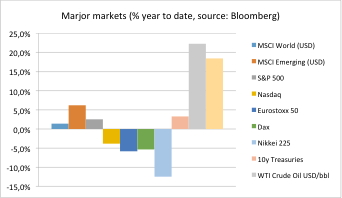

Most stock markets have pared losses from their drop earlier this year. Year-to-date the S&P 500 just reached positive territory, MSCI Emerging Markets index is even better. Europan markets are still slightly lower than at the beginning of the year and Japan is even in the double-digit area negative.

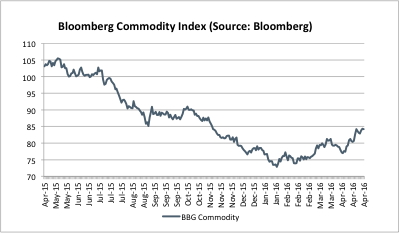

The winners are commodities by far. Crude oil has bottomed out and is +22%, Gold is +18%, other energy and metals are similar. For a nice summary see Bloomberg commodity index as our chart of the day!

Where to we go from here? Current earnings season is mixed. On average broad markets lack growth. Both sales and earnings report signal a total decline for European and the US companies. Valuations are rather high compared to their own history. S&P 500 is trading at 19x reported earnings and EuroStoxx 50 at 22x. Analysts still factor in considerable growth for current and next year which could be a base for disappointments.

However the key driver keeps central bank policy. Mario Draghi is still expanding monetary base in Euro area. Bank of Japan does it the sometimes faster, this week slower than expected. On the other hand US Fed is still hesitant on its opposite path. While some ‘experts’ expect the second US rate hike for June of this year market prices reflect a probability of 14% only for Fed meeting in June. However by December of this year there is a probability of 63% for higher US rates.

The upcoming Brexit vote might cause some extra turbulences – see also our special on this http://www.innovatis-suisse.ch/investmentblog-on-upcoming-brexit-vote/

Thus Erwin Lasshofer and his INNOVATIS team expect limited upside and more volatility ahead. We prefer income oriented structured notes to benefit from volatile sideways markets. Don’t hesitate to contact us for investment solutions that meet your needs.

Archives

- June 2019 (1)

- March 2019 (1)

- February 2019 (1)

- December 2018 (1)

- May 2018 (1)

- January 2018 (1)

- December 2017 (2)

- October 2017 (1)

- September 2017 (1)

- August 2017 (1)

- July 2017 (1)

- June 2017 (2)

- May 2017 (2)

- April 2017 (2)

- March 2017 (3)

- February 2017 (2)

- January 2017 (2)

- December 2016 (4)

- November 2016 (3)

- October 2016 (3)

- September 2016 (2)

- August 2016 (5)

- July 2016 (2)

- June 2016 (4)

- May 2016 (1)

- April 2016 (4)

- March 2016 (5)

- February 2016 (3)

- January 2016 (3)

- December 2015 (5)

- November 2015 (5)

- October 2015 (4)

- September 2015 (3)

- August 2015 (7)

- July 2015 (7)

- June 2015 (5)

- May 2015 (6)

- April 2015 (9)

- March 2015 (9)

- February 2015 (9)

- January 2015 (9)

- December 2014 (11)

- November 2014 (10)

- October 2014 (3)

- September 2014 (1)

- August 2014 (2)

- July 2014 (2)

Related Posts

Investmentblog on upcoming Brexit vote

By Erwin Lasshofer

What is ahead? On 23 June 2016 the United Kingdom will hold a referendum on the country’s membership of the EU. The name combines ‚Britain‘ and ‘Exit’ According to latest polls about 38% will vote to leave, 42% to stay and 20% do not know yet. A leave vote would trigger a […]

READ MORE

Newsletter dated April 13, 2016

By Erwin Lasshofer

Are you following INNOVATIS on Facebook, Linked-In& Co. yet? You can find Erwin Lasshofer and his INNOVATIS Team on major social media platforms such as Facebook Linked-In XING Google+ We post company news and recommend links to investment related readings here. Below you find a selection of recent recommendations. […]

READ MORE